You are using an outdated browser. Please upgrade your browser to improve your experience.

Article | 04 July 2024 | Investments

Rémi Lambert

Chief Investment Officer

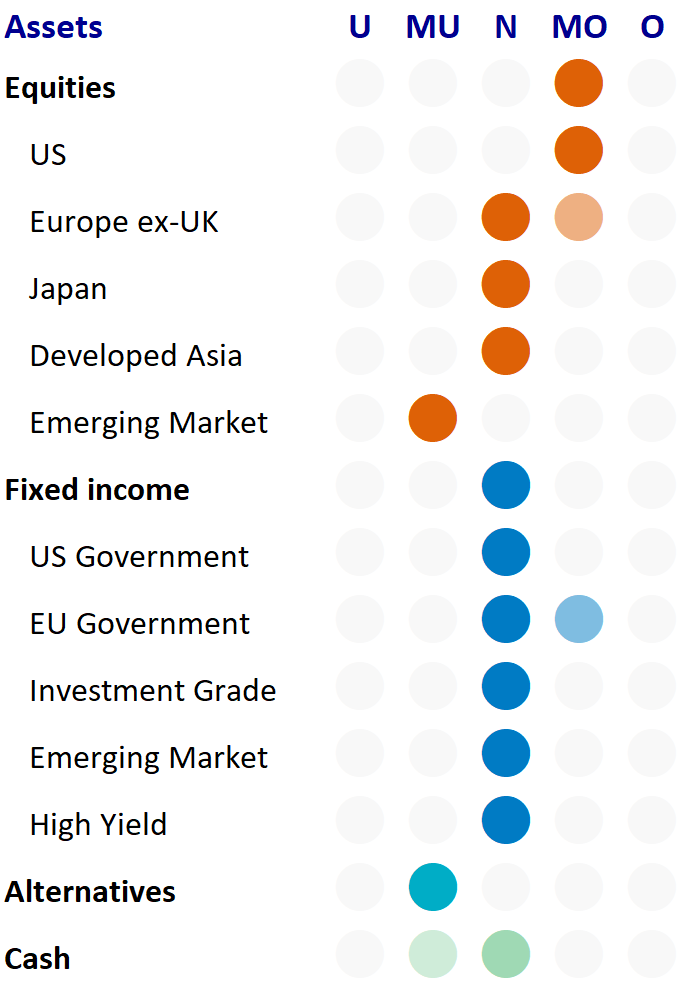

U = Underweight, MU = Moderate underweight, N = Neutral, MO = Moderate overweight, O = Overweight

100% colour circle (⬤) = Current positioning

50% colour circle (⬤) = Previous positioning

Source: AXA IM Select, as at 30 June 2024.

For illustrative purposes only.

June was an eventful month, marked by elections in Europe, India, Mexico, and South Africa. Populist promises and fiscally loose plans have fuelled debate and raised the risk of re-igniting inflation. The European Central Bank (ECB) and the Bank of Canada cut interest rates, while undertaking to closely monitor both inflation and labour market data. As expected, the US Federal Reserve (Fed) did not cut rates in June and advised patience in the face of “a number of upside inflation risks”.

Equity markets have continued to progress, driven by the US and its technology sector. Nvidia briefly became the most valuable company in the world. Global emerging markets also touched new highs, driven by both India and Taiwan over the last quarter. Within fixed income, government bonds and credit markets have delivered positive returns at the margin, albeit with some intra-month volatility. The US dollar remains well supported, especially versus the euro and the Japanese yen, on expectations of higher for longer interest rates. Oil prices rose 5.8% to close at $86.40 a barrel. Copper prices fell sharply amid concerns over the growth outlook, particularly in China.

We continue to expect a soft landing over the coming year, as inflation slowly returns to the 2-3% targets set by central banks and global growth remains resilient. Given the current macroeconomic regime, we continue to prefer equities over bonds and alternative assets, with US equities our main preference. We are maintaining, but not increasing, our US equity exposure. Despite tighter valuations and narrow market leadership in the US, earnings growth momentum remains positive. We expect another positive earnings season, with Q2 releases starting in early July.

We have cut our European equity exposure to neutral, expressing a preference for ex-Eurozone markets within the region. We maintain a neutral position in Japanese equities. The Bank of Japan is likely to tighten policy further and to repeat interventions in support of the yen. This could create new sources of volatility after a strong performance over the last year. We remain slightly negative on emerging market equities, concerned by property market developments and slow consumption growth in China. Additionally, tensions around tariffs on trade with Europe and the US have increased. Uncertainties around elections within core emerging markets are resolving, however, which might lead us to reassess our position.

We are downgrading our fixed income exposure to neutral, remaining cautious about the fallout from the French elections. German bonds might continue to benefit from a flight to quality, although fiscal policies could hinder future price appreciation. We expect the ECB to cut rates two more times this year, as wage growth and inflation should move lower. Given historically low credit spreads and better upside for equity markets, we remain neutral on developed market investment grade and high yield bonds, as well as emerging market debt.

As a result, the cash and alternative assets exposure of our TAA model portfolio increases. We believe that active managers should perform well in this environment.